Making your way on to the property ladder has long-been considered a worthy ambition for young people in the UK.

As well as being a fantastic investment, that all-important first purchase increases equity, allowing for more property purchases down the line.

But with prices rising every year, and wages barely keeping up, today’s UK housing market is especially tough for first-time buyers.

To make matters worse, on April 1 2025, the stamp duty threshold will be lowered from £425,000 to £300,000 – meaning first-time buyers previously exempt from the tax will have to cough up an additional £5,000 on first homes.

The maximum purchase price for those wishing to claim the reduced First-Time Buyers Relief, currently £625,000, will also now return to the previous rate of £500,000.

But despite these challenging conditions, first-time buyers remain ‘the driving force of the housing market,’ according to Richard Donnell, head of research and insight at Zoopla.

With the help of estate agents Benham and Reeves, we’ve gathered all of the latest data from the Office of National Statistics and spoken to property experts to compile the ultimate affordability guide in the UK, including the most and least affordable destinations, and the schemes available to give a helping hand.

MARKET REALITIES

As of July 2024, 53 per cent of adults in the UK own their homes, a noticeable decline in the last few decades. 66 per cent of the population were homeowners back in 1991.

This rate has fallen most significantly for those aged 25-34. In 2011, the average first-time buyer was 29-years-old. Today you’re more likely to be 33 when bagging the keys to your first home.

But it’s not all bad news. According to Andrew Harvey, senior economist at Nationwide, we entered 2025 with ‘modest improvement’ in the UK housing affordability rates, ‘due to earnings growth marginally outpacing house price growth and a slight reduction in average borrowing costs.’

He also points out things are looking up for first-time buyers, whose share of house purchase mortgages was ‘higher in 2024 (54 per cent) than it was pre-pandemic (51 per cent)’.

Richard Donnell echoes his optimism, observing that the 2025 sales market is off to a stronger start than the past two years, with 22 per cent of renters looking to become buyers for the first time either now, or in the next two years.

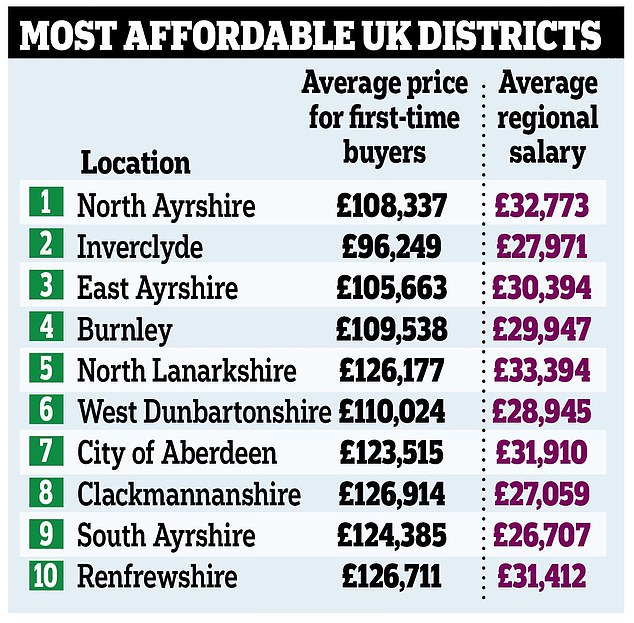

MOST AFFORDABLE

Inevitably, you get more bang for your buck depending on where in the country you decide to buy.

Typically, lenders determine what you can afford using a loan-to-income ratio, based on four to four-and-a-half times one’s average salary, and a deposit of approximately 10 per cent of the property’s total value.

Scotland’s North Ayrshire – a 45 minute drive from Glasgow – is the most affordable place for first-timers to buy. With average salaries of £32,773 and prices at £108,337, it boasts an attractive 3.3 affordability ratio.

North Ayrshire, near Glasgow, is the most affordable place for first-timers to buy

In Burnley, the most affordable district in England, the affordability ratio for first-time buyers is 3.37 – well below the recommended 4 to 4.5

Wrexham, in Wales, (the ‘happiest’ place to live according to Rightmove) has a 5.6 affordability ratio

In London, Croydon is your best bet, with an 9.1 affordability ratio, based on an average first-time buyer price of £347,439

In Burnley, the most affordable district in England, the affordability ratio for first-time buyers is 3.37 – well below the recommended 4 to 4.5. To buy your first home here, you would need a salary of approximately £24,900 – below the regional average of £29,947 – with a 10 per cent deposit of around £12,800.

Wrexham – the ‘happiest’ place to live according to Rightmove – has a 5.6 affordabability ratio, making it much more affordable than other Welsh cities, such as Cardiff and Swansea, which sit at 7.87 and 6.61 respectively.

For those wishing to buy in the capital, Croydon is your best bet, with an 9.1 affordability ratio, based on an average first-time buyer price of £347,439 and an average regional salary of £38,020.

LEAST AFFORDABLE

Unsurprisingly, London is the least affordable place in the UK to buy property for the first time. With an affordability ratio of 20.83, a 10 per cent deposit for a first-time buyer in Kensington and Chelsea would cost approximately £92,400, with standard mortgage rates demanding an annual salary of a whopping £205,271 – at the very least.

With an affordability ratio of 20.83, a 10 per cent deposit for a first-time buyer in Kensington and Chelsea would cost approximately £92,400, with standard mortgage rates demanding an annual salary of a whopping £205,271 (Pictured: South Kensington)

To buy in St Albans, Hertfordshire, where the average price for a first-time buyer is £485,335, a standard 10 per cent deposit would be approximately £48,500, and the required annual salary a minimum of £97,000

Even in areas like Trafford, where the average first-time property price is lower (£321,000), the 9.4 affordability ratio remains steep

Reflecting its proximity to London, parts of Hertfordshire are similarly eye-watering. To buy in St Albans, where the average price for a first-time buyer is £485,335, a standard 10 per cent deposit would be approximately £48,500, and the required annual salary a minimum of £97,000.

Even in areas further north, like Trafford, where the average first-time property price is lower (£321,000), the 9.4 affordability ratio remains steep. Based on the common mortgage lending, buying in Trafford would require an annual salary of around £62,657 – well above the district’s average of approximately £33,200.

RENTAL WOES

The Office of National Statistics recently revealed the average rent in the UK was £1,326 per month in February 2025. This is £99 – 8.1 per cent – higher than this time last year. Savills forecast a further 17.6 per cent increase between 2025 and 2029.

It’s no wonder, then, young people want to get themselves on to the ever-slippery property ladder.

Renting a two-bed property in Kensington and Chelsea is £3,358 per month on average (Pictured: Earl’s Court)

In Cambridge, rent for a two-bed property costs £1,568 every month – over half of the average person’s monthly salary

Renting a two-bed property is £2,521 in Islington, north London

For those in the capital, the cost of rent is significantly higher. Renting a two-bed property in Kensington and Chelsea is £3,358 per month on average, and £2,521 in Islington, north London.

But even outside of London, rent is becoming untenable. In Cambridge, rent for a two-bed property costs £1,568 every month – over half of the average person’s monthly salary.

The situation does not improve vastly further north, where traditionally the cost of living has been cheaper. In Manchester, the average rent for a two-bed is £1,177, totalling roughly 40 per cent of a person’s average annual salary.

The knock-on effect of this rental crisis is not just the impact on renters’ lifestyle, but their ability to save towards a first deposit. According to Richard Donnell those on low-to-middle range salaries will ‘really struggle’ to do so without financial support, and notes many more young people are choosing to live with family as opposed to renting, to help save for that first deposit.

Inevitably, you get more bang for your buck depending on where in the country you decide to buy. Here is a handy list of the most affordable places in the UK to buy

SCHEMES TO HELP

Until June 30 this year, you can apply for the Government-backed ‘Mortgage Guarantee Scheme’ to buy any home for under £600,000. The scheme has lenders offer 95 per cent mortgages, meaning buyers only need five per cent deposits to buy property.

The Government acts as a guarantor for 15 per cent of the mortgage, so will cover the shortfall for that portion if buyers default on their payments. While it’s aimed at first-time buyers, these 95 per cent mortgages are available to anyone.

The ‘First Homes Scheme’ also helps local first-time buyers and key workers onto the property ladder, offering a 30 to 50 per cent discount on new-build homes.

To be eligible for this scheme, you must earn under £80,000 per year (£90,000 In London), and the property you’re buying must cost no more than £250,000 (£420,000 in London).

The scheme requires an active connection with the area you wish to buy in, such as growing up there or working locally, and prioritises key workers.