Gambling hedge funds and the threat of China dumping US debt have been blamed for market chaos that forced Donald Trump‘s humiliating tariffs climbdown.

The US president executed an extraordinary U-turn by pausing the bulk of his ‘Liberation Day’ levies on trading partners for three months.

That sparked a brief but massive relief rally on Wall Street yesterday – and temporarily eased huge pressure on US Treasury bonds.

The interest rates on those ‘notes’ are critical as they are used to finance the American government’s eye-watering debt pile, as well as borrowing rates for ordinary citizens.

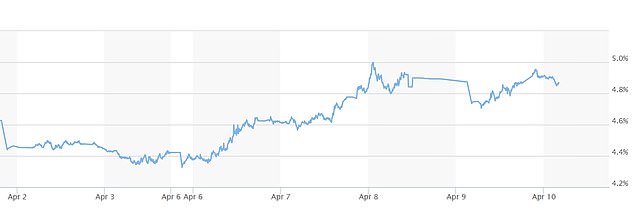

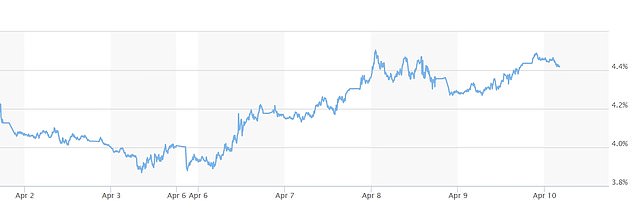

However, the US Treasuries selloff picked up pace during Asian trading hours overnight. The ten-year ‘note’ yield hit 4.45 per cent, up nearly half a percentage point over the week – the biggest increase since 2001.

Analysts and investors have pointed to the selloff in Treasuries and the falling US dollar as a sign of faltering confidence in the world’s biggest economy.

Concerns have also been running high that China could unload some of its mountain of US debt as the trade war with Mr Trump escalates.

However, the finger has also been pointed at hedge funds ‘leveraging’ to stake bets on the bond market.

On another grim day of global carnage:

- China has announced that tariffs on US imports are being raised to 125 per cent in the latest tit-for-tat;

- UK ministers have admitted that a deal might not be reached with the US to get rid of 10 per cent tariffs;

- EU commission president Ursula von der Leyen has threatened a fresh tax on American big tech firms if the US does not agree to drop tariffs permanently.

Donald Trump has executed an extraordinary U-turn by pausing the bulk of his ‘Liberation Day’ levies on trading partners for three months

The yield on 30-year US Treasury bonds has been rising alarmingly this week

The 10-year US Treasury bonds have also risen sharply as the chaos over Trump’s tariffs rages

So-called ‘basis trades’ see hedge funds engage in heavy short-term borrowing in an effort to exploit small differences between US bond prices and their values on the ‘futures’ market.

When they were caught out by the wider fire sale in bonds, the funds were forced to sell to close their positions rather than racking up enormous losses.

One former senior Bank of England policymaker told the Times that central banks must do more to restrain the practice.

‘Regulators are not doing enough with respect to containing leverage,’ the source said. ‘The US is moving in the opposite direction, and other central banks are being bamboozled by their own banks to follow.’

The Bank of England warned in November of the risk that a ‘market shock’ could cause rapid ‘de-leveraging’ in US Treasury bonds.

Analysts have been warning that the US is far from out of the woods despite Mr Trump appearing to back off most of his tariffs.

The US president covered his wider reverse by ratcheting up tariffs on Chinese imports to an effective 145 per cent.

China has hit back, hiking its tariffs on the US with each Trump increase, raising fears that Beijing may jack up duties above the current 84 per cent.

Kyle Rodda, senior financial markets analyst at Capital.com said: ‘There’s clearly an exodus from U.S. assets. A falling currency and bond market is never a good sign.

‘This goes beyond pricing in a growth slowdown and trade uncertainty.’

Global stocks fell and the dollar sank further overnight, although the FTSE 100 clawed back a bit more ground in early trading this morning.

The anxiety has sparked a rush into safe havens, sending the Swiss franc soaring to a decade high against the dollar, and gold to a new peak.

In Asia, Japan’s Nikkei tumbled 4.3 per cent on the day, while stocks in South Korea fell nearly 1 per cent. Taiwan’s main index reversed earlier losses to trade nearly 2 per cent higher.

In contrast, Chinese stocks have been holding relatively steady. The blue-chip CSI300 Index was 0.1 per cent lower while Hong Kong’s benchmark Hang Seng rose 0.56 per cent.