Nearly £175 billion has been wiped off the UK stock market in just a week – hammering the pensions and savings of millions.

As the market meltdown triggered by Donald Trump‘s trade war accelerated, the FTSE 100 suffered its sharpest drop since the outbreak of the pandemic.

The punishing rout, which was echoed from Wall Street to Asia, came after Mr Trump slapped drastic tariffs on trading partners, fuelling fears of a worldwide recession. Analysts warned that the rout threatened to scupper retirement plans for those hoping to claim their pension within the next few years.

As global markets took a £4.4 trillion hit this week, Wall Street giant JP Morgan warned: ‘There will be blood.’

The investment bank said the chances of a global recession have spiked from 40 per cent to 60 per cent after Mr Trump imposed a 10 per cent baseline tariff on all imports to the US. Some countries were hit with higher levies of up to 50 per cent, sending shockwaves through global markets.

The rout intensified yesterday after Beijing retaliated with 34 per cent levy on imported American goods, with the stand-off between the two largest economies bringing the world closer to a full-blown trade war.

Fears that other nations will impose tit-for-tat tariffs in the coming days stoked the panic spreading through markets.

Writing on his Truth Social platform, Mr Trump insisted: ‘China played it wrong, they panicked – the one thing they cannot afford to do.’

The London stock exchange crashed this week after President Trump announced a wide-ranging series of tariffs on goods entering the US

The president unveiled the tariffs on a country-by-country basis in the White House Rose Garden

Mr Trump also unveiled a new ‘gold card’, a US residency permit for foreigners costing $5 million (£3.9 million). He showed off a prototype of the ‘Trump Card’ to reporters aboard his presidential jet Air Force One

He said the sharp drop in share prices was a buying opportunity for investors. It’s a ‘great time to get rich, richer than ever before,’ the President said as he vowed his ‘policies will never change’.

Mr Trump also unveiled a new ‘gold card’ yesterday, a US residency permit for foreigners costing $5 million (£3.9 million). He showed off a prototype of the ‘Trump Card’ to reporters aboard his presidential jet Air Force One.

After plunging 1.5 per cent on Thursday, the FTSE 100 index of blue-chip companies fell 4.9 per cent yesterday – the sharpest drop in five years.

The domestically focused FTSE 250 was down 4.4 per cent and the FTSE all-share index, which tracks around 600 London-listed companies, tumbled 4.87 per cent. In total £173.5 billion has been wiped off the index’s value over the week.

Analysts warned that the huge sell off will hammer pensions and savings. ‘For those still a few years away from retirement, market volatility could be a real concern,’ said Myron Jobson, senior personal finance analyst at UK stockbroker Interactive Investor.

‘An extended downturn in equities could significantly dent the value of their pension pots just as they’re preparing to draw on them. This, in turn, threatens to scupper plans for retirement.

‘For retirees relying on investment growth, a weaker stock market could mean their savings don’t stretch as far as planned.’

Dan Coatsworth, an investment analyst at AJ Bell, said British savers should ‘focus on the long term and not lose confidence’ and that ‘the turmoil caused by tariffs and fears of a global trade war is not a reason to stop investing’.

President Trump holds aloft a signed executive order implementing his new regime of tariffs

The president gave a long and wide-ranging speech as he laid out his philosophy on trade

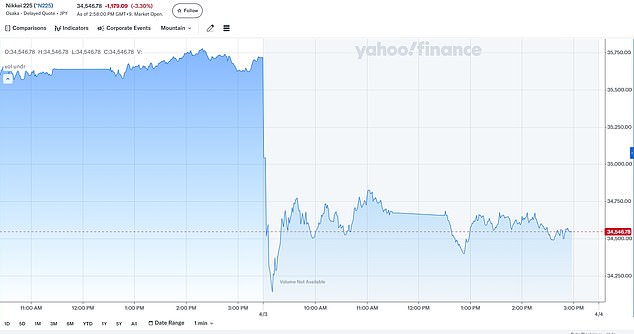

The Japanese Nikkei fell off a cliff as it opened following Mr Trump’s tariffs blitz

EU commission president Ursula von der Leyen said the bloc is ‘finalising’ its initial retaliation

Business chiefs in No10 earlier this week to discuss the new tariff regime included AstraZeneca ‘s Pascal Soriot, BAE’s Charles Woodburn and Jaguar Land Rover’s Richard Molyneux

Tremors were felt across global markets, with European stocks taking another battering while nursing losses from earlier in the week. The Europe-wide Stoxx 600 fell a further 5.2 per cent after a 2.6 per cent drop on Thursday.

In Frankfurt, the Dax fell 4.66 per cent and the CAC 40 in Paris dropped 4.26 per cent. Milan’s FTSE MIB tumbled 6.53 per cent while the Ibex 35 in Madrid slumped 5.8 per cent.

Wall Street was also hammered on Friday, with the benchmark S&P 500 index dropping as much as 3.8 per cent and the Dow Jones Industrial Average falling 3.4 per cent.

The tech-focused Nasdaq Composite tumbled 3.98 per cent after around 5 per cent was wiped off its value on Thursday.

The index was down more than 20 per cent from its recent record high, entering what investors call a ‘bear market’.

The carnage on American markets also hurt British savers, as many people have a portion of their pension and other investments tied up in US stocks.

A sharp drop in US prices was a ‘good reminder to have a diversified portfolio’, AJ Bell’s Mr Coatsworth said.

The CBOE Volatility index, known as Wall Street’s fear gauge, hit its highest level since August 2024 at 37.66 points.

‘A lot of investors I’ve talked to have just said in this kind of environment, let’s go to cash and just wait it out,’ Rick Meckler, a partner at family investment office Cherry Lane Investments, said.

Keir Starmer admitted pain is looming as he met business leaders in Downing Street on Thursday

Chancellor Rachel Reeves has acknowledged that the UK will not be ‘out of the woods’ even if it can get exemptions from their US counterparts

‘The market is pricing in a global recession,’ added George Saravelos, global head of FX research at Deutsche Bank.

Asian shares crumbled overnight on Thursday after the continent was slapped with some of Trump’s highest levies.

Tokyo’s Nikkei crashed 2.75 per cent, Hong Kong’s Hang Seng fell 1.52 per cent and China’s Shanghai Composite dropped 0.24 per cent.