THE average two-year fixed mortgage rate has dropped below the average five-year fixed rate for the first time since Liz Truss’ mini-Budget.

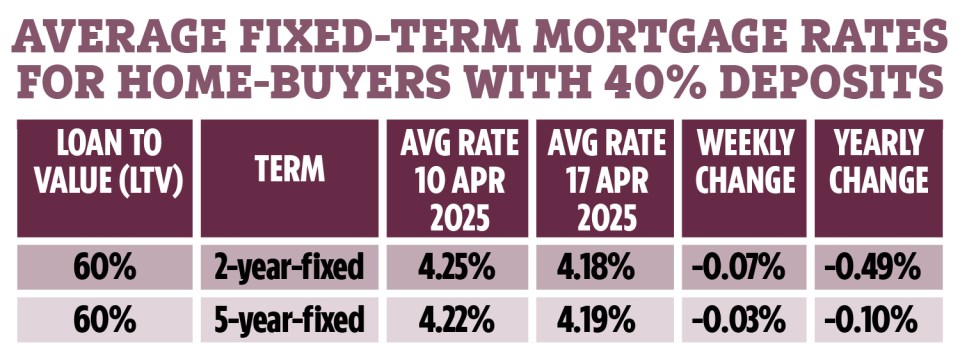

The average two-year fixed mortgage rate for those with a 40% deposit is now 4.18% while the average five-year fixed mortgage rate for those with a 40% deposit is 4.19%, according to Podium.

3

3

Meanwhile, the lowest available two-year fixed rate is now 3.86%, while the lowest available five-year fixed rate is 3.89%.

Nick Mendes, mortgage technical manager at John Charcol, said the shift had come with interest rates set to fall quicker than expected over the next two years.

Most economists were already expecting rates to be cut in May and now many think there will be four in total this year.

It comes as economic uncertainty caused by Trump’s trade tariffs mean interest rates may need to be slashed to encourage growth.

Nick said: “This shift reflects expectations that interest rates might start coming down over the next couple of years.

“The global tariffs situation, among other economic signals, has accelerated this trend, suggesting lenders believe rates may ease sooner rather than later.”

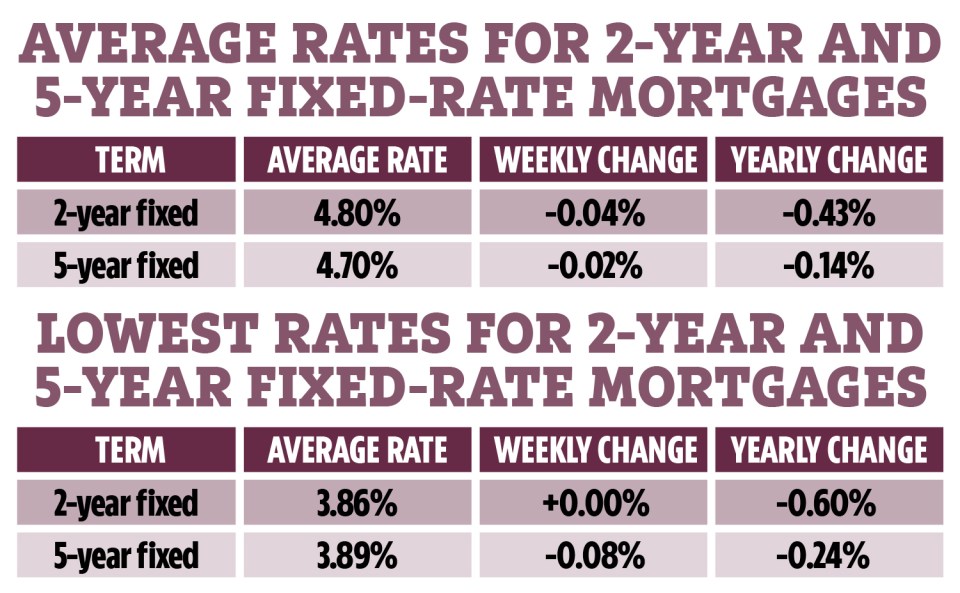

The latest data from Podium also reveals the gap between the average two-year fixed rate and five-year fixed rate is also closing.

However, mortgage rates with 40% deposits are the first product bracket to have cheaper average two-year rates since Liz Truss‘ mini-Budget in October 2022.

For example, the average rate for a two-year fixed deal with a 5% deposit is 5.54%, down 0.03% from 5.57% in the week commencing April 7.

But this is in comparison to 5.35% for a five-year fixed deal with a 5% deposit, up from 5.34% in the week commencing April 7.

Meanwhile, the average rate for a two-year fixed deal with a 10% deposit is 5.09%, down 0.05% from 5.14% in the week commencing April 7.

This is in comparison to 4.86% for a five-year fixed deal with a 10% deposit, down from 4.89% in the week commencing April 7.

Matt Smith, mortgage expert at Rightmove, said average mortgage rates across the board should follow two-year fixed deals over the coming months in falling though.

“Mass-market average rate trends should gradually follow, and a Bank Rate cut in May will give lenders some more headroom for further rate cuts.”

3

Is it worth fixing for two years?

It could be depending on whether you want to benefit from cheaper monthly repayments in the short term.

Expectations of a base rate cut in May and a further three later this year could mean interest rates are lower when you come to signing up for a new deal in two years’ time.

However, there is no certainty over what will happen to interest rates so you may come to sign a new deal in two years and find you’re paying more.

Nick, from John Charcol, explained: “If you’re confident in your income and plan to review things in a couple of years, a two-year deal might be a sensible option, especially as those rates are currently slightly lower.

“It gives you flexibility and the potential to benefit from falling rates in the near future.

“However, if you value stability and want to protect against the risk of future rate rises, a five-year fix offers more peace of mind.

“It may be a touch more expensive now, but it can save stress later on.”

Nick said it can be worth looking at three-year fixed rate deals too, as these offer you both flexibility and stability.

He added: “Three-year mortgage deals have traditionally flown a little under the radar, sitting quietly between the more common two and five-year options.

“But recently, we have started to see more attractive rates being offered in this space, and that is making borrowers take a second look.

“If you are not quite ready to commit to a five-year deal but feel that two years is just a bit too short, then a three-year option could be a perfect middle ground.”

Anyone not sure on what to do next can speak to a mortgage broker to weigh up their options.

But be aware they may charge you a fee for their services, with the average cost around 0.35% up to 1% of the loan size.

Others may charge you a flat fee for their services.

How to get the best deal on your mortgage

IF you’re looking for a traditional type of mortgage, getting the best rates depends entirely on what’s available at any given time.

There are several ways to land the best deal.

Usually the larger the deposit you have the lower the rate you can get.

If you’re remortgaging and your loan-to-value ratio (LTV) has changed, you’ll get access to better rates than before.

Your LTV will go down if your outstanding mortgage is lower and/or your home’s value is higher.

A change to your credit score or a better salary could also help you access better rates.

And if you’re nearing the end of a fixed deal soon it’s worth looking for new deals now.

You can lock in current deals sometimes up to six months before your current deal ends.

Leaving a fixed deal early will usually come with an early exit fee, so you want to avoid this extra cost.

But depending on the cost and how much you could save by switching versus sticking, it could be worth paying to leave the deal – but compare the costs first.

To find the best deal use a mortgage comparison tool to see what’s available.

You can also go to a mortgage broker who can compare a much larger range of deals for you.

Some will charge an extra fee but there are plenty who give advice for free and get paid only on commission from the lender.

You’ll also need to factor in fees for the mortgage, though some have no fees at all.

You can add the fee – sometimes more than £1,000 – to the cost of the mortgage, but be aware that means you’ll pay interest on it and so will cost more in the long term.

You can use a mortgage calculator to see how much you could borrow.

Remember you’ll have to pass the lender’s strict eligibility criteria too, which will include affordability checks and looking at your credit file.

You may also need to provide documents such as utility bills, proof of benefits, your last three month’s payslips, passports and bank statements.

Do you have a money problem that needs sorting? Get in touch by emailing money-sm@news.co.uk.

Plus, you can join our Sun Money Chats and Tips Facebook group to share your tips and stories